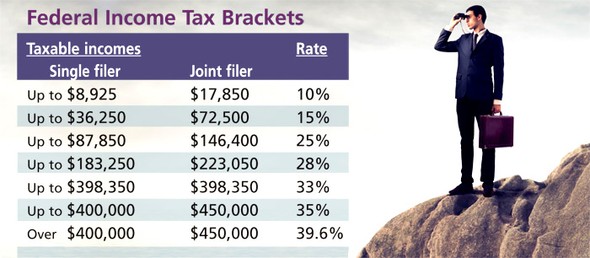

More than one-third of retirees lack confidence that they will have enough money to live comfortably throughout their retirement years.1 Committing to a savings strategy during your working career could go a long way to help alleviate this concern, but it’s also important to make sound decisions when withdrawing assets from the portfolio you worked so hard to accumulate.

The 4% Solution

One common approach has been to withdraw 4% of your portfolio in the first year of retirement, with inflation-adjusted amounts in subsequent years. The so-called “4% rule” was developed in the 1990s using historical market research, and it was based on a 30-year retirement with savings in a tax-deferred account and nothing left for heirs.2

Lately, in response to a concern that future market returns might be lower than historical averages, some retirees have reduced their initial withdrawals to 3% or 3.5%.3 By contrast, more optimistic or aggressive investors and those who can rely on a traditional pension for some income might begin with a higher withdrawal rate.

The Three-Phase Solution

An alternative approach if you live or plan to live in Charleston SC, Charlotte NC, Miami FL or Atlanta GA is to envision a three-phase retirement and divide your investment assets into three pools that reflect the needs, risk level, and growth potential of each phase. In the first pool you might hold cash and cash alternatives; in the second you could have mostly fixed-income securities, such as bonds; and in the third you could have growth-oriented investments such as stocks that might be more volatile but have higher growth potential over the long term.

For the first five years or so, you might receive income primarily from assets in the first pool. For the middle phase, five to 15 years in the future, you would have income from the second pool of assets. And during the third phase, more than 15 years in the future, you would have income from growth-oriented investments.

Throughout your retirement you could periodically shift assets from the long-term pool to the shorter-term pools so that you would continue to have mid-term and short-term funds available (see accompanying illustration).

Some retirees might be more comfortable having targets for specific investments and dividing a long-term strategy into more manageable segments. However, this method also depends on market performance, and if assets for one pool are depleted earlier than planned, you may have to draw on assets from the next pool.

All investments are subject to market fluctuation, risk, and loss of principal. Investments, when sold, and bonds redeemed prior to maturity may be worth more or less than their original cost. Asset allocation is a method used to help manage investment risk; it does not guarantee against investment loss.

The most appropriate distribution strategy for your own retirement income depends on many factors, such as the size and performance of your portfolio, as well as your risk tolerance, lifestyle goals, health, and life expectancy. Balancing these and other factors can be daunting, and you may benefit from professional guidance.

Although there is no assurance that working with a financial advisor will improve investment results, a professional who focuses on your overall objectives can help you consider options that could have a substantial effect on your long-term financial situation.

1) Employee Benefit Research Institute, 2012

2) smartmoney.com, February 7, 2012

3) InvestmentNews, January 23, 2012

2) smartmoney.com, February 7, 2012

3) InvestmentNews, January 23, 2012

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. Copyright © 2013 Emerald Connect, Inc.

Click here for more Newsletters. Thank you.

Miami FL, Charleston SC, Atlanta GA, Charlotte NC - Tax, Financial Planning, Investments & Insurance.