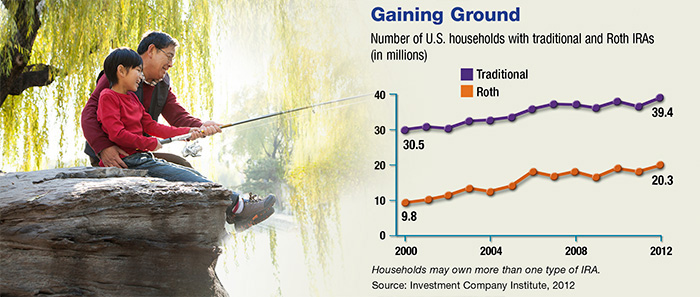

Second thoughts are part of life, which may explain why some investors change their minds about the types of accounts they use for retirement savings in Charleston SC, Charlotte NC, Miami FL and Atlanta GA. This could be the case for traditional and Roth IRAs, which feature different tax treatments of contributions and distributions.

The IRS allows taxpayers to convert traditional IRA assets to a Roth IRA — and even to recharacterize (revert assets back to a traditional IRA) under certain conditions. Until recently, however, assets in employer-sponsored 401(k), 403(b), and governmental 457(b) plans could be converted to a Roth account only if they were considered distributable assets. This typically applied to people who had assets in a former employer’s plan as well as those aged 59½ and older.

The American Taxpayer Relief Act of 2012 provides a new opportunity to convert tax-deferred employer plan assets — including 401(k), 403(b), and 457(b) plans — to a Roth account offered by the same employer. Unlike Roth IRA conversions, however, in-plan Roth conversions are irrevocable and cannot be recharacterized.

Taxed Now or Later

Traditional IRAs and most employer-sponsored plans offer a current-year tax deduction for contributions, up to annual limits. However, distributions — including contributions and any earnings — are taxed as ordinary income. By contrast, contributions to a Roth account are not deductible. However, qualified withdrawals are generally free of federal income tax as long as they meet certain conditions (discussed below).

Traditional IRAs and most employer-sponsored plans offer a current-year tax deduction for contributions, up to annual limits. However, distributions — including contributions and any earnings — are taxed as ordinary income. By contrast, contributions to a Roth account are not deductible. However, qualified withdrawals are generally free of federal income tax as long as they meet certain conditions (discussed below).

Conversions of tax-deferred assets (from an employer’s retirement plan or a traditional IRA) to a Roth account are subject to federal income taxes in the year of the conversion. Under current tax law, if all conditions are met, the Roth account will incur no further income tax liability for the rest of the owner’s lifetime or for the lifetimes of the owner’s designated beneficiaries, regardless of how much growth the account experiences.

The prospect of a substantial tax bill can be daunting, but trading current-year liability for tax-free income in retirement may be appealing if you expect to be in the same or a higher tax bracket in retirement, if you have unusually low income during a particular year, or if you want to take advantage of potential earnings growth free of federal income taxes. Conversions can be spread over a number of years, which may make the tax liability more manageable.

To qualify for the tax-free and penalty-free withdrawal of earnings, a Roth account must meet the five-year holding requirement and the distribution must take place after age 59½ or result from certain conditions such as the owner’s death, disability, or a first-time home purchase ($10,000 lifetime maximum).

Required minimum distributions from traditional IRAs and most employer-sponsored plans (including Roth employer plans) must begin by April 1 of the year following the year in which you turn age 70½. There are no mandatory distribution requirements from Roth IRAs. Beneficiaries of IRAs and employer-sponsored retirement plans are required to take mandatory distributions based on their own life expectancies.

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Brinker Capital.

Click here for more Newsletters. Thank you.

Miami FL, Charleston SC, Atlanta GA, Charlotte NC - Tax, Financial Planning, Investments & Insurance.

Connect and Read More About Us

Hedges Wealth Management LLC - A Registered Investment Adviser

Hedges Insurance Agency LLC

Tax, Financial Planning, Investments & Insurance Advisors

1300 Appling Drive #201 | Mt Pleasant | SC 29464

T | F 704 919 5946

If you are looking for more information on any subject in this Blog, please Contact Us directly electronically or via phone. Thank you.